-

Top 10 Year End Financial Review Tips

Year End Financial Review is important as the year draws to a close, it’s not only a time for holiday celebrations and reflecting on personal growth but also an excellent opportunity to conduct a thorough review of your financial health.

Year End Financial Review is important as the year draws to a close, it’s not only a time for holiday celebrations and reflecting on personal growth but also an excellent opportunity to conduct a thorough review of your financial health. The Top 10 Year End Financial Review Tips guide is here to assist you in this essential process.

This comprehensive financial check-up is like an annual performance evaluation for your finances, allowing you to take a closer look at your monetary goals, accomplishments, and hurdles from the past year while preparing for the challenges and opportunities that the next year may bring.

Whether you’re a seasoned investor, a diligent saver, or someone just beginning their financial journey, this guide is a valuable resource. It offers a holistic approach to financial review, covering a range of key areas such as budget management, investment assessment, retirement planning, tax optimization, and more. By following these tips, you can gain a deeper understanding of your financial landscape, make informed decisions, and ensure that your financial strategies align with your long-term goals. So, let’s embark on this financial journey together, and equip ourselves with the knowledge and tools needed to take control of our financial future.

.

Financial Year End Tools

Whether you’re a seasoned financial guru or just beginning your journey to financial literacy, exploring these tools can be a game-changer in achieving your monetary objectives. Some tools for your end of year review

Budget Planner

Budget Planner This is a comprehensive budget planner that is aimed in saving money and repaying debt fast

- Monthly bill organizer with pockets

- Expense tracker and finance journaling

- Financial calendar that tracks spending & savings

- 4 pages for debt tracking, 2 pages for Holiday budgeting,

- 2 pages for regular bill tracking, and 2 pages for annual

.

Personal Finance Book

Personal Finance BookThis book showcases how to completely transform your finances by showing step by step strategies

- Simplified beginners guide to eliminate financial stress

- Comes with digital simplified templates to use

- Saving strategies that can quickly save money

- Debt paying strategies that will erase debt faster

.

.

Retirement Planning Guidebook

Retirement Planning GuidebookThis guidebook certainly helps in laying a strong foundation.

- Assess where you wish to live in retirement

- Manage your long-term care risk between self-funding

- Investment and insurance tools that fit your personal style

- Make smart decisions for when to start Social Security benefits

- Determine if you are financially prepared for retirement by quantifying your financial goals

.

Cashflow Quadrant Guide

Cashflow Quadrant GuideThe first book was Rich Dad Poor Dad. This is the

second book which reveals how the 1 percent manage, grow, protect their assets such as:- How to work less, earn more, pay less in taxes

- Book is written for those needed to secure financial freedom

- Showcases the different methods how to achieve financial freedom

- Highlights how to strategically move beyond job security and acquire financial literacy

..

1 Review Your Budget and Expenses

Reviewing your budget and expenses is a fundamental step in your year-end financial review. As the year comes to a close, it’s essential to assess your financial health and ensure that your spending aligns with your financial goals. Take a close look at your budget to evaluate how well you’ve adhered to your spending plan throughout the year. Analyze your monthly expenses, and identify any areas where you may have overspent or encountered unexpected costs. By pinpointing these financial patterns, you can make informed decisions about adjustments for the coming year. It’s also an excellent time to assess your subscriptions, discretionary spending, and potential cost-cutting measures to optimize your budget. This meticulous examination of your budget and expenses forms the foundation for a successful financial review, helping you identify areas for improvement and set the stage for a financially secure future.

.

2. Assess Your Debt Situation

Assessing your debt situation is a critical component of your year-end financial review. It’s essential to understand the impact of your outstanding debts on your overall financial health. Begin by compiling a list of all your debts, including credit card balances, loans, mortgages, and any other liabilities. Take note of the interest rates, minimum payments, and the total amount owed for each debt. With this comprehensive overview, you can assess the progress you’ve made in reducing your debts throughout the year and make informed decisions about your debt management strategy for the future. By evaluating your debt situation, you can identify opportunities to accelerate debt repayment, refinance high-interest loans, or consolidate debts to reduce your financial burden. The goal is to create a clear path towards debt reduction, helping you achieve greater financial freedom and peace of mind in the year ahead.

.

3. Check Your Credit Report

Checking your credit report is a crucial element of your year-end financial review. Your credit report serves as a snapshot of your financial history and plays a significant role in your financial well-being. By obtaining a copy of your credit report from the major credit bureaus, you can review your credit history, ensure its accuracy, and identify any potential issues that may need your attention. Look for discrepancies, errors, or signs of identity theft that could adversely affect your credit score. Addressing these issues promptly can safeguard your financial reputation and ensure that your credit remains in good standing. A healthy credit report can lead to better lending opportunities, lower interest rates, and increased financial flexibility in the future. Therefore, as you conduct your year-end financial review, don’t overlook the importance of monitoring and maintaining a strong credit history.

.

4. Reevaluate Your Investments

Reevaluating your investments is a critical step in your year-end financial review, as it allows you to assess the performance of your investment portfolio and make informed decisions for the future. Begin by reviewing the performance of your investments, including stocks, bonds, mutual funds, and any other assets in your portfolio. Analyze the gains and losses, paying particular attention to the overall return on your investments. Consider your investment goals and risk tolerance to determine whether your current portfolio aligns with your financial objectives. If necessary, rebalance your portfolio to maintain the desired asset allocation and diversify your investments for a more stable and resilient financial future. Additionally, take the opportunity to assess your investment fees and expenses, ensuring that you are not paying more than necessary. By reevaluating your investments, you can optimize your portfolio, make necessary adjustments, and set a course for achieving your long-term financial goals with confidence.

.

5. Update Retirement Contributions

Updating your retirement contributions is a pivotal component of your year-end financial review, as it enables you to secure your financial future with prudent retirement planning. Start by assessing your current retirement account contributions, including 401(k), IRA, or other retirement savings vehicles. Review your contribution limits and compare them to your actual contributions to determine if there’s room for improvement. Increasing your contributions before the year’s end can offer immediate tax benefits and enhance your long-term retirement savings. Additionally, if you receive an employer match in your workplace retirement plan, ensure that you are contributing enough to maximize this valuable benefit. If you’ve experienced changes in your financial situation, such as a pay raise or a financial windfall, consider allocating some of the extra income toward your retirement accounts. By updating your retirement contributions, you are taking a proactive step toward building a more secure and comfortable retirement, making the most of the available tax advantages, and increasing your financial well-being in the years to come.

.

6. Plan for Tax Efficiency

Planning for tax efficiency is a vital aspect of your year-end financial review, and it can significantly impact your overall financial well-being. As the year draws to a close, it’s a prime time to explore tax-saving opportunities. Begin by evaluating your current tax situation, taking into account your income, deductions, and any life changes that may affect your tax liability. Look for strategies to reduce your taxable income, such as maximizing contributions to tax-advantaged accounts, like a 401(k) or IRA. Consider charitable donations or other tax-deductible expenses that could lower your tax bill. Moreover, explore tax-loss harvesting opportunities to offset capital gains and reduce your overall tax liability. By planning for tax efficiency, you can make the most of available tax breaks, minimize your tax burden, and allocate more of your hard-earned money toward your financial goals, whether that’s saving for retirement, investing in your future, or enjoying more financial flexibility.

.

7. Examine Your Emergency Fund

Examining your emergency fund is a vital step in your year-end financial review, as it serves as a financial safety net that can provide security and peace of mind. As the year comes to a close, it’s a perfect time to assess the status of your emergency fund. Consider your current financial situation and whether any changes have occurred throughout the year. Evaluate the size of your emergency fund and ensure that it aligns with your needs and financial obligations. Experts typically recommend having three to six months’ worth of living expenses saved in your emergency fund. If your fund falls short of this goal, consider increasing your contributions to it in the upcoming year. An adequately funded emergency fund can protect you from unexpected expenses, such as medical bills, car repairs, or job loss, allowing you to maintain financial stability and avoid accumulating debt during challenging times. By examining and strengthening your emergency fund during your year-end financial review, you are enhancing your financial resilience and preparing for any unexpected events that may arise in the future.

.

8. Update Insurance Coverage

Updating your insurance coverage is an important component of your year-end financial review, as it ensures that you have adequate protection for life’s unexpected events. Take the time to review all of your insurance policies, including health, auto, home or renters, and life insurance. Consider whether any changes in your life, such as marriage, having a child, or purchasing a new home, may necessitate adjustments to your coverage. Ensure that your policies offer the right level of protection and that they align with your current needs and financial situation. This review is also an opportunity to explore potential cost savings, like bundling home and auto insurance or raising deductibles to lower premiums. By updating your insurance coverage, you can safeguard your financial security and protect your loved ones, giving you peace of mind in the face of life’s uncertainties.

.

9. Estate Planning and Legal Documents

Estate planning and reviewing legal documents are essential tasks in your year-end financial review that may often be overlooked. Take time to review your will, trusts, power of attorney, and any other legal documents that outline your wishes regarding your assets and healthcare decisions. Ensure that these documents are up to date and accurately reflect your current circumstances and wishes. If you’ve experienced significant life changes, such as marriage, divorce, or the birth of a child, it’s crucial to update your legal documents accordingly. Estate planning is not only about securing your assets for the future but also ensuring that your loved ones are provided for and that your healthcare preferences are respected. By addressing these matters during your year-end financial review, you can have peace of mind, knowing that your affairs are in order and that your financial and personal wishes will be honored in the years to come.

.

10. Set New Financial Goals

Setting new financial goals is a central element of your year-end financial review, as it provides you with a roadmap for your financial future. Reflect on your current financial situation, accomplishments, and any challenges you’ve faced throughout the year. Based on these insights, identify areas in which you’d like to make improvements or where you see opportunities for growth. Your financial goals may vary, from saving for a specific purchase or vacation to increasing your retirement contributions, reducing debt, or expanding your investment portfolio. Setting well-defined and achievable financial goals not only motivates you but also helps you maintain financial discipline. As the new year approaches, consider your short-term and long-term objectives, create an action plan to achieve them, and set benchmarks to measure your progress along the way. By establishing new financial goals in your year-end review, you’re empowering yourself to make purposeful financial decisions and work toward the future you envision.

.

Conclusion

A year-end financial checkup is an essential exercise to assess your financial health and set the stage for a prosperous financial future. By examining your budget, debt, investments, and insurance, you can ensure that your financial well-being remains on track. Remember to consult relevant tools and resources, and consider professional advice when necessary to make the most informed decisions.

.

-

10 Lucrative Fall Investments in Autumn

These lucrative fall investments are best bought in the fall as they will yield more.

These lucrative fall investments are best bought in the fall as they will yield more. As autumn leaves begin to fall, astute investors know that this season can bring unique opportunities for lucrative investments. The financial landscape often undergoes significant changes during the fall months, offering the chance to diversify your portfolio and maximize your returns.

In this blog post, we’ll explore 10 fall investments that have historically proven to be lucrative, along with examples and relevant site links to guide you in your investment journey. Autumn is a season of transformation, a time when nature’s vibrant colors and cool breezes signal change. It’s also a season of opportunity for investors looking to capitalize on unique trends and seasonal opportunities. While fall investments may not be as widely discussed as those associated with other times of the year, they can be just as lucrative.

From capitalizing on holiday shopping trends to considering investments in sectors like energy, agriculture, and more, there’s a range of investment opportunities ripe for the picking. In this guide, we’ll explore ten fall investments that have the potential to yield significant returns and why autumn is an ideal time to consider them. Whether you’re a seasoned investor or just getting started, these insights will help you make the most of the financial opportunities the fall season has to offer.

.

1. Autumn Harvest Investments: Agriculture Stocks

- As fall approaches, consider investing in agriculture stocks, such as Archer-Daniels-Midland (ADM) or Deere & Company (DE). These stocks can benefit from increased demand for fall harvests and seasonal trends in food production.

As autumn sets in, the world of agriculture undergoes a profound transformation. It’s harvest season, a time when farmers reap the fruits of their labor, and the markets respond to the abundance of crops. For investors, this season presents a unique opportunity to consider agriculture stocks as a potentially lucrative investment. Agriculture stocks can offer an appealing blend of stability and growth potential, and they tend to thrive during the fall season. In this segment of our guide on fall investments, we will delve into the world of agriculture stocks and explore why they become particularly attractive during this time of the year. By understanding the dynamics of this sector and the seasonal factors at play, you can make informed decisions on how to potentially yield fruitful returns from your investments this autumn.

.

2. Energy Sector: Heating Oil Futures

- The demand for heating oil tends to rise as temperatures drop in the fall. Investing in heating oil futures, available through platforms like the Intercontinental Exchange (ICE or CME Group, can be a strategic move.)

As the leaves change and the temperature drops, the energy sector experiences a significant shift in demand, particularly in the form of heating oil. Autumn marks the beginning of the heating season, when households and businesses start relying on heating systems to keep warm. Seasonal change translates into an opportunity to consider heating oil futures as a potentially lucrative investment. Energy sector investments, and specifically heating oil futures, become particularly attractive during the fall season due to increased demand and the unique market dynamics that accompany it. By understanding the intricacies of this sector and its seasonal factors, you can make informed investment decisions to potentially warm up your portfolio during the fall.

.

3. Real Estate: Fall Home Sales

- Historically, the fall season has seen increased real estate activity as families look to move before the holidays. Consider investing in Real Estate Investment Trusts (REITs) like Realty Income Corporation (O) or explore residential real estate opportunities.

Real estate markets across the country experience their own shift during the fall months, making it an interesting time for investors to consider the lucrative opportunities within the housing sector. Fall is often associated with increased home sales, presenting an attractive opportunity for those looking to invest in real estate. Whether you’re an experienced investor or just dipping your toes into the world of property investment, understanding the unique dynamics of fall home sales can provide you with valuable insights and the potential to capitalize on this seasonal trend.

.

4. Technology: E-commerce Stocks

- With the holiday shopping season on the horizon, e-commerce companies like Amazon (AMZN) tend to see increased demand and higher stock valuations in the fall.

The holiday season, a time when shopping activity surges. For investors, this season presents an exceptional opportunity to consider e-commerce stocks as a potentially lucrative investment, which fall under the technology sector. E-commerce has been reshaping the retail landscape, and the fall season, with Black Friday and Cyber Monday as its crescendo, holds a significant share of this digital commerce surge. As consumers increasingly turn to online shopping for their holiday needs, e-commerce stocks become particularly attractive during this time of year. Understanding the dynamics of this sector and the seasonal trends at play can help you make informed investment decisions to potentially reap the rewards this fall season.

.

5. Consumer Goods: Beverage Companies

- Fall is often associated with cozy beverages. Investing in beverage companies, such as Starbucks (SBUX) or Coca-Cola (KO), can be a wise choice due to higher consumption during the season.

As the air turns crisp and leaves begin to fall, consumer behaviors also undergo a seasonal shift, creating unique opportunities for investors. Among these shifts, autumn ushers in a particular fondness for warm beverages and festive drinks. The season presents an exciting opportunity to consider investments in beverage companies, which often experience heightened demand during the fall months. Consumer goods, specifically beverage companies, can offer an appealing mix of stability and growth potential, especially in the lead-up to the holiday season. Understanding the dynamics of this sector and the seasonal factors at play, you can make informed decisions to potentially yield a refreshing return on your investments this fall.

.

6. Travel Industry: Airline and Hotel Stocks

- With students returning to school and less summer travel, the fall can be a great time to invest in airline and hotel stocks. Companies like Delta Air Lines (DAL) or Marriott International (MAR) can be attractive investments.

Autumn, with its mild weather and the anticipation of holiday travel, brings a fresh breeze of opportunity to the travel industry. This season marks a window of potential profitability, as it’s a time when airline and hotel stocks often experience a surge in demand. With families planning trips to reunite with loved ones during the holidays and travelers seeking autumn getaways, the travel industry tends to thrive during this season.

.

7. Healthcare: Flu Season and Pharmaceutical Stocks

- Flu season typically arrives in the fall, leading to increased demand for healthcare services and pharmaceuticals. Consider investing in healthcare stocks, including companies like Pfizer (PFE) or Johnson & Johnson (JNJ).

As the leaves fall and temperatures dip, another seasonal change begins to take shape – the arrival of flu season. With people looking to protect themselves and their families from the seasonal influenza, healthcare and pharmaceutical companies often experience an increase in demand for flu vaccines and related medications. For investors, this presents a valuable opportunity to consider pharmaceutical stocks as a potentially lucrative investment. The fall season brings with it a renewed focus on health and wellness, making it a prime time for the pharmaceutical sector.

.

8. Gold and Precious Metals

Precious metals, particularly gold, are often considered safe-haven assets. As market volatility may increase during the fall, investing in gold or exchange-traded funds (ETFs) like SPDR Gold Trust (GLD) can provide stability to your portfolio.

The fall season often brings about unique opportunities, and one that shines particularly bright is the realm of precious metals, especially gold. As the holiday season approaches and economic dynamics shift, gold and other precious metals tend to become even more appealing as an investment choice. Their historical value and reputation as safe-haven assets make them an attractive option for those looking to diversify their portfolio.

.

9. Insurance Companies: Hurricane Season

Fall marks the peak of hurricane season, making it a strategic time to invest in insurance companies, which may experience increased premiums and demand for coverage. Notable examples include Progressive Corporation (PGR) and Allstate Corporation (ALL).

The fall season brings a heightened awareness of the potential for extreme weather events, particularly hurricanes. For investors, this time presents a unique opportunity to consider investments in insurance companies, which play a crucial role in mitigating the financial impact of such disasters. As hurricane season continues into the fall, the demand for insurance coverage tends to rise. By understanding the dynamics of this sector and the seasonal factors at play, you can make informed investment decisions to potentially weather the storms and secure your financial future this fall

.

10. Renewable Energy Stocks: Green Investments

- Investing in renewable energy stocks, such as NextEra Energy (NEE) or First Solar (FSLR), can be a forward-thinking choice. Fall can bring increased attention to sustainability and clean energy initiatives.

It’s a time when the energy landscape also undergoes a transformation, with the focus shifting towards sustainable and renewable sources of power. For investors, this season offers an exceptional opportunity to consider investments in renewable energy stocks as a potentially lucrative choice. As the world becomes increasingly conscious of the need for eco-friendly alternatives and sustainable practices, the fall season often sees a surge in interest in renewable energy.

.

Conclusion

Investing in the fall season offers opportunities to capitalize on seasonal trends and market shifts. Whether you opt for agriculture stocks, heating oil futures, or e-commerce companies, it’s crucial to conduct thorough research and consider your own financial goals and risk tolerance. The examples and site links provided in this blog post can serve as valuable starting points for your investment journey during this lucrative autumn season. Remember to consult with a financial advisor for personalized investment advice.

.

-

10 Best Investing Strategies for Beginners

Investing Strategies for Beginners includes researching the best method for your financial goals as well as taking charge when it comes to becoming financially literate.

Investing Strategies for Beginners includes researching the best method for your financial goals as well as taking charge when it comes to becoming financially literate.Investing can be a powerful tool for building wealth and securing your financial future, but for beginners, it can also be a daunting endeavor. The world of investments is vast and complex, filled with a multitude of options and strategies.

In this blog post it explores ten of the best investing strategies tailored for beginners. From understanding the principles of diversification and risk management to exploring investment vehicles like stocks, bonds, and exchange-traded funds (ETFs), these strategies are designed to provide a solid foundation for those who are new to the world of investing.

Whether your financial goals involve saving for retirement, buying a home, or simply growing your wealth, these insights will equip you with the knowledge and tools necessary to embark on your investing journey with confidence and set the stage for a more secure financial future. So, let’s embark on this educational journey to discover the ten best investing strategies for beginners and open the door to the world of financial opportunity.

.

1. Understand the Purpose of Investing

Investing involves putting your money into assets with the expectation of generating a return over time. The primary goals of investing include building wealth, beating inflation, funding retirement, and achieving financial independence. By investing wisely, you can make your money work for you and potentially earn more than traditional savings accounts or other low-yield options.

Investing in stocks can provide capital appreciation and dividend income, while real estate investments can generate rental income and potential property value appreciation. By understanding the purpose of investing, you can align your strategies and decisions with your long-term financial goals, whether it’s saving for retirement, funding your children’s education, or building a safety net for unforeseen circumstances.

.

2. Define Your Investment Goals

Before you start investing, it’s crucial to establish clear investment goals. Determine your financial objectives, such as buying a home, funding education, saving for retirement, or building a nest egg. Setting specific and measurable goals will guide your investment decisions and help you stay focused throughout your investing journey.

- For instance, one goal may be to build a retirement nest egg that will provide financial security in your golden years. This could involve long-term investments with a focus on wealth accumulation and capital appreciation. Another goal could be saving for a down payment on a house or funding your child’s education. In this case, a mix of medium-term investments with moderate risk could be appropriate.

By defining your investment goals, you can establish a roadmap that guides your investment decisions, asset allocation, and risk management strategies, helping you achieve the financial future you desire.

.

3. Educate Yourself

Investing requires knowledge and understanding of various concepts, strategies, and investment options. Take the time to educate yourself on the basics of investing. When it comes to investing, knowledge is power.

- Educating yourself can be beneficial in understanding different asset classes and staying up-to-date with economic news and trends. By learning about stocks, bonds, mutual funds, real estate, and other investment vehicles, you can diversify your portfolio and make informed investment choices.

- Additionally, keeping abreast of economic indicators, industry news, and geopolitical events can help you anticipate market movements and adjust your investment strategy accordingly. Remember, investing is a continuous learning process, and the more you educate yourself, the better equipped you’ll be to navigate the ever-changing investment landscape.

Knowledge is your best ally when it comes to making informed investment decisions. Read books, articles, and reputable websites dedicated to investing. Familiarize yourself with key terms such as stocks, bonds, mutual funds, diversification, risk tolerance, and asset allocation.

.

4. Determine Your Risk Tolerance

Risk tolerance refers to your ability and willingness to endure the ups and downs of the investment markets. Consider your financial situation, time horizon, and personal comfort level with volatility.

- Generally, younger individuals with a longer time horizon can afford to take on more risk, while those nearing retirement might opt for more conservative investments. Understanding your risk tolerance will help you choose appropriate investment vehicles.

By understanding your risk tolerance, you can tailor your investment strategy to align with your comfort level, financial goals, and time horizon, ultimately increasing the likelihood of achieving your investment objectives.

.

5. Start with a Solid Financial Foundation

Before diving into investing, establish a solid financial foundation. Pay off high-interest debt, build an emergency fund, and create a budget to manage your expenses. Investing should be a part of a well-rounded financial plan and not a substitute for addressing essential financial obligations.

Two key components of building a solid foundation are creating a budget and establishing an emergency fund.

- Firstly, creating a budget allows you to gain a clear understanding of your income, expenses, and financial goals. It helps you track your spending, identify areas where you can save, and allocate funds towards your priorities, including investments. By having a budget in place, you can make informed decisions about how to allocate your resources and ensure that you’re living within your means.

- Secondly, establishing an emergency fund is essential for handling unexpected financial setbacks. Life is full of uncertainties, and having a financial safety net can provide you with peace of mind. Aim to save three to six months’ worth of living expenses in an easily accessible account. This fund will serve as a cushion during challenging times, such as job loss, medical emergencies, or unexpected repairs.

By starting with a solid financial foundation, you set yourself up for success in your investment journey. Budgeting helps you prioritize your financial goals and manage your cash flow effectively, while an emergency fund provides a safety net and prevents you from relying on debt in times of crisis. These foundational steps lay the groundwork for building wealth and achieving financial stability over the long term.

.

6. Diversify Your Portfolio

Diversification is a key risk management strategy in investing. It involves spreading your investments across different asset classes, industries, and geographical regions. By diversifying, you can reduce the impact of any single investment’s performance on your overall portfolio. Consider allocating your investments among stocks, bonds, real estate, and other asset classes based on your risk tolerance and investment goals.

- One example of diversification is investing in a mix of stocks, bonds, and cash equivalents. Stocks offer the potential for higher returns but also come with higher risk, while bonds provide stability and income. By having a balanced allocation between these asset classes, you can benefit from both growth potential and income generation while managing risk.

- Another example of diversification is investing across various sectors or industries. Different sectors perform differently under various market conditions. By diversifying across sectors such as technology, healthcare, finance, consumer goods, and others, you reduce the concentration risk of being heavily exposed to a single sector. This way, if one sector experiences a downturn, the performance of your portfolio won’t be solely dependent on it.

Diversification helps to smooth out the ups and downs of the market and increase the likelihood of consistent returns over time. By spreading your investments across different asset classes and sectors, you can potentially reduce the overall volatility of your portfolio and increase the chances of capturing gains in different areas of the market.

.

7. Choose the Right Investment Accounts

Selecting the right investment accounts is crucial for tax efficiency and optimizing your investment returns. Common investment accounts include individual retirement accounts (IRAs), employer-sponsored 401(k) plans, and brokerage accounts. Research the advantages, contribution limits, and tax implications of each account type to determine which ones align with your financial goals.

- An IRA is a tax-advantaged retirement account that allows individuals to save for retirement. There are different types of IRAs, such as Traditional IRAs and Roth IRAs. Traditional IRAs offer potential tax deductions on contributions, while Roth IRAs provide tax-free withdrawals in retirement. Choosing the appropriate IRA based on your income, tax situation, and retirement goals can help you maximize your retirement savings and potentially reduce your tax liability.

- A 401(k) plan is an employer-sponsored retirement account offered by many companies. It allows employees to contribute a portion of their pre-tax salary towards retirement savings. One of the key advantages of a 401(k) is the potential for employer matching contributions, which is essentially free money. By participating in your employer’s 401(k) plan and taking full advantage of the matching contributions, you can significantly boost your retirement savings.

By carefully selecting the right investment accounts based on your financial goals and tax considerations, you can take advantage of specific benefits and features that align with your investment strategy and optimize your overall investment returns.

.

8. Start Small and Consistently Invest

When starting as a beginner investor, it’s wise to start small and gradually increase your investment contributions over time. Consider setting up automatic contributions from your bank account to your investment accounts. Consistency is key, as it allows you to benefit from dollar-cost averaging, where you buy more shares when prices are low and fewer shares when prices are high.

Consistently investing, regardless of market fluctuations, allows you to take advantage of dollar-cost averaging, where you buy more shares when prices are lower and fewer shares when prices are higher. This approach can help smooth out the impact of market volatility and potentially increase your long-term returns.

- For example, you can start with a systematic investment plan (SIP) in mutual funds, where you invest a fixed amount regularly, such as monthly or quarterly. By investing a consistent amount at regular intervals, you can take advantage of market fluctuations and potentially accumulate a significant investment portfolio over time.

- Another example is setting up an automatic investment plan where you designate a certain portion of your income to be automatically invested in a diversified portfolio. This ensures that you consistently invest without the need for manual intervention, making it easier to stick to your investment strategy.

By starting small and consistently investing, you can build a solid foundation for your investment journey and benefit from the power of compounding over time. It allows you to develop good investing habits, mitigate the impact of market volatility, and steadily grow your investment portfolio.

.

9. Monitor and Rebalance Your Portfolio

Regularly monitor the performance of your investments and review your portfolio’s allocation. Over time, certain investments may outperform or underperform, causing your asset allocation to deviate from your intended targets. Periodically rebalance your portfolio by buying or selling investments to restore your desired asset allocation.

- If your target allocation is 60% stocks and 40% bonds, and due to market performance, your stocks have grown to 70% of your portfolio, you may need to sell some stocks and purchase bonds to rebalance back to your desired allocation. This helps maintain the desired risk-reward profile of your portfolio.

- Monitoring the performance of individual investments within your portfolio. If certain investments consistently underperform or no longer align with your investment thesis, you may need to consider replacing them with better alternatives. This proactive monitoring allows you to optimize your portfolio and make informed decisions to maximize returns and minimize risks.

By monitoring and rebalancing your portfolio, you can ensure that it remains aligned with your investment goals, risk tolerance, and market conditions. Regularly reviewing your portfolio allows you to make necessary adjustments, capitalize on opportunities, and mitigate potential risks, thereby increasing the likelihood of achieving your long-term financial objectives.

.

10. Seek Professional Advice if Needed

If you feel overwhelmed or lack the time and expertise to manage your investments, consider seeking professional financial advice. Financial advisors can provide personalized guidance, help you set realistic goals, and design an investment strategy tailored to your needs. However, do thorough research and choose a reputable advisor who acts in your best interest.

- For example, if you’re unsure about the best asset allocation for your investment goals or need assistance in selecting specific investments, a financial advisor can provide expert advice based on their knowledge and experience. They can help you develop a customized investment strategy that aligns with your objectives, time horizon, and risk tolerance.

- If you have a complex financial situation, such as multiple income sources, estate planning considerations, or tax implications, seeking professional advice can help you navigate these complexities. An advisor can provide valuable insights on tax-efficient investment strategies, retirement planning, or legacy planning to ensure your investments are optimized and aligned with your broader financial objectives.

By seeking professional advice when needed, you can benefit from their expertise and experience, gaining valuable insights and ensuring your investment decisions are well-informed and aligned with your financial goals. Remember to choose a reputable and qualified professional who can provide personalized advice based on your unique circumstances.

.

Conclusion

In conclusion, investing can be an effective way to grow your wealth and achieve your financial goals. As a beginner, it’s important to approach investing with a solid foundation of knowledge and a well-defined strategy. By understanding the purpose of investing, defining your investment goals, educating yourself about different investment options, and determining your risk tolerance, you can make informed decisions that align with your financial objectives.

Starting with a small investment, diversifying your portfolio, choosing the right investment accounts, and consistently monitoring and rebalancing your investments can help you build a strong investment portfolio over time. If needed, seeking professional advice can provide valuable insights and guidance tailored to your unique circumstances. Remember that investing involves risks, and it’s essential to stay disciplined, patient, and adaptable to market conditions. With time, patience, and a commitment to learning, you can embark on a successful investing journey and work towards achieving your financial aspirations.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest |

.

-

7 Different Types of Insurance and Why You Need Them

There are Different Types of Insurance which serves as a crucial financial safety net, providing protection and peace of mind in the face of unexpected events.

There are Different Types of Insurance which serves as a crucial financial safety net, providing protection and peace of mind in the face of unexpected events.Understanding the various types of insurance and their importance is essential for safeguarding yourself, your loved ones, and your assets.

Insurance plays a crucial role in protecting individuals, businesses, and their assets from various risks and uncertainties. From safeguarding your health to protecting your property, there are numerous types of insurance available to mitigate potential financial losses.

In this guide, we will delve into some of the most common types of insurance, exploring their purpose, benefits, and considerations. Whether you are looking to protect your health, home, vehicle, or other valuable assets, gaining knowledge about the various types of insurance will empower you to make informed choices and effectively manage potential risks. In this blog post, we will explore different types of insurance and explain why having adequate coverage is a wise decision.

.

1. Health Insurance

Health insurance is vital for managing medical expenses and ensuring access to quality healthcare. It covers a portion of medical costs, including doctor visits, hospitalization, medications, and preventive services. Health insurance protects you from financial burdens associated with medical emergencies and allows you to receive necessary medical care without worrying about exorbitant bills.

- Managing Healthcare Expenses: Health insurance typically involves some level of cost-sharing, such as deductibles, copayments, and coinsurance. Understand your financial responsibilities and budget accordingly. Consider setting up a health savings account (HSA) or a flexible spending account (FSA) if available, as these can help you save money specifically for healthcare expenses on a tax-advantaged basis

.

2. Auto Insurance

Auto insurance is a legal requirement in most places and provides financial protection in case of accidents, theft, or damage to your vehicle. It typically covers liability (injury or property damage to others), collision (damage to your car), and comprehensive (non-collision-related damage) aspects. Auto insurance not only protects your investment in your vehicle but also safeguards you from potential liability claims.

- Coverage Options: Auto insurance typically offers different types of coverage, including liability coverage, collision coverage, comprehensive coverage, uninsured/underinsured motorist coverage, and medical payments coverage.

- Liability coverage is usually required by law and covers damages you cause to other people or property in an accident. Collision coverage helps cover the costs of repairing or replacing your vehicle in the event of a collision.

- Comprehensive coverage protects against non-collision-related damages, such as theft, vandalism, or natural disasters. Uninsured/underinsured motorist coverage provides protection if you’re involved in an accident with a driver who doesn’t have sufficient insurance. Medical payments coverage helps pay for medical expenses resulting from an accident.

.

3. Homeowner’s or Renter’s Insurance

Homeowner’s insurance is essential if you own a home, while renter’s insurance is crucial for those living in rented properties. These types of insurance protect your dwelling or personal belongings against damage or loss due to events like fire, theft, vandalism, or natural disasters. Additionally, they provide liability coverage in case someone is injured on your property. Homeowner’s or renter’s insurance safeguards your home or belongings, allowing you to recover financially from unforeseen incidents.

- Coverage for Property: Homeowner’s insurance covers the physical structure of your home, as well as any detached structures on your property, such as a garage or shed. It also provides coverage for your personal belongings inside the home, including furniture, electronics, appliances, and clothing. Renter’s insurance, on the other hand, covers the tenant’s personal property inside the rented premises.

- Liability Coverage: In addition to property coverage, homeowner’s and renter’s insurance policies typically include liability coverage. This protects you financially if someone is injured on your property and files a lawsuit against you. It helps cover medical expenses, legal fees, and other costs associated with such claims.

- Additional Living Expenses: Homeowner’s and renter’s insurance policies may also include coverage for additional living expenses. If your home becomes uninhabitable due to a covered event, such as a fire or natural disaster, this coverage helps pay for temporary housing, meals, and other expenses until your home is repaired or you find a new place to live.

.

4. Life Insurance

Life insurance offers financial protection for your loved ones in the event of your death. It provides a lump sum payment (the death benefit) to your beneficiaries, which can be used to replace lost income, cover funeral expenses, pay off debts, or secure their financial future. Life insurance is particularly crucial if you have dependents, outstanding debts, or financial obligations that would burden your loved ones upon your passing.

- Death Benefit: The primary purpose of life insurance is to provide a death benefit to your beneficiaries upon your death. This lump-sum payout can help cover various expenses, including funeral costs, outstanding debts, mortgage payments, education expenses, and ongoing living expenses for your family.

- Types of Life Insurance: There are different types of life insurance policies available, including term life insurance and permanent life insurance. Term life insurance provides coverage for a specific period, typically 10, 20, or 30 years. It offers a death benefit if you pass away during the term of the policy. Permanent life insurance, such as whole life or universal life insurance, provides coverage for your entire life and also includes a cash value component that grows over time.

- Assessing Your Needs: When determining the amount of life insurance coverage you need, consider factors such as your income, debts, financial obligations, and the future needs of your dependents. Assessing your needs can help you determine the appropriate coverage amount and policy type.

.

5. Disability Insurance

Disability insurance protects your income if you become unable to work due to a disability or illness. It provides a percentage of your pre-disability income, ensuring you have a source of funds to cover daily expenses and maintain your standard of living. Disability insurance is important because a loss of income due to a disability can have a significant impact on your financial well-being and long-term financial goals.

- Income Replacement: Disability insurance provides a portion of your income in the event that you are unable to work due to a disability. It helps cover your daily living expenses, such as mortgage or rent payments, utility bills, groceries, and other financial obligations.

- Short-term and Long-term Coverage: Disability insurance policies can be categorized into short-term and long-term disability coverage. Short-term disability insurance typically covers a portion of your income for a limited period, such as three to six months. Long-term disability insurance, on the other hand, provides coverage for an extended period, ranging from several years to until retirement age, depending on the policy.

- Own-Occupation vs. Any-Occupation: When selecting a disability insurance policy, it’s important to consider whether it provides coverage based on an own-occupation or any-occupation definition. Own-occupation coverage pays benefits if you are unable to perform the duties of your specific occupation, while any-occupation coverage pays benefits only if you are unable to work in any occupation for which you are reasonably qualified.

.

6. Umbrella Insurance

Umbrella insurance offers additional liability protection beyond the coverage limits of your auto, homeowner’s, or renter’s insurance policies. It provides an extra layer of financial protection against lawsuits, medical expenses, or property damage claims that exceed your primary policy’s limits. Umbrella insurance is valuable for individuals who desire increased liability coverage, particularly those with significant assets or higher-risk professions.

- Increased Liability Coverage: Umbrella insurance provides additional liability coverage above and beyond the limits of your primary insurance policies. It helps protect you from potential lawsuits and claims that exceed the liability limits of your home or auto insurance. This coverage is designed to protect your assets, such as your savings, investments, and property, in the event of a significant liability claim.

- Wide Range of Coverage: Umbrella insurance offers broader coverage compared to your primary insurance policies. It not only extends the liability coverage for your home and auto but also covers other areas of your life, such as rental properties, boats, and recreational vehicles. It may also provide coverage for certain personal liabilities, such as libel, slander, or defamation.

- Cost-Effective Protection: Umbrella insurance is typically affordable considering the substantial coverage it offers. The cost of an umbrella policy is relatively low compared to the potential financial impact of a lawsuit or liability claim. By having umbrella insurance, you can mitigate the risk of personal financial loss due to costly legal judgments or settlements.

.

7. Long-Term Care Insurance

Long-term care insurance covers the costs associated with long-term care services, such as nursing homes, assisted living facilities, or in-home care. It provides financial assistance for individuals who require assistance with daily activities due to age, illness, or disability. Long-term care insurance can help preserve your savings and assets while ensuring you receive the necessary care and support..

- Coverage for Long-Term Care Services: Long-term care insurance is designed to cover the costs of services required for assistance with activities of daily living (ADLs) or chronic medical conditions. These services can include nursing home care, assisted living facilities, in-home care, and adult daycare. Having long-term care insurance can help alleviate the financial burden of these services, which can be significant and often not covered by traditional health insurance or Medicare.

- Asset Protection: One of the primary benefits of long-term care insurance is asset protection. Without coverage, the cost of long-term care services can quickly deplete your savings and assets. By having long-term care insurance, you can help preserve your wealth and ensure that it is not exhausted by the high costs associated with long-term care.

- Flexibility and Customization: Long-term care insurance policies offer flexibility in terms of coverage options and benefit amounts. You can customize your policy based on factors such as the type of services you want covered, the benefit period, and the daily benefit amount. It’s important to review and understand the policy terms, including any waiting periods, elimination periods, and limitations on coverage.

.

Conclusion

Insurance is not just an additional expense but a wise investment in your financial security and protection. Understanding the different types of insurance and their significance allows you to make informed decisions about the coverage you need. Whether it’s health, auto, homeowner’s, life, disability, umbrella, or long-term care insurance, each serves a specific purpose in safeguarding your finances, assets, and loved ones. By having appropriate insurance coverage, you can face unexpected events with confidence, knowing that you have a safety net to support you.

.

Cheering To Your Success

Brenda | www.DesignYourFinances.com

Let’s Connect on Social Media! | Pinterest |

.

-

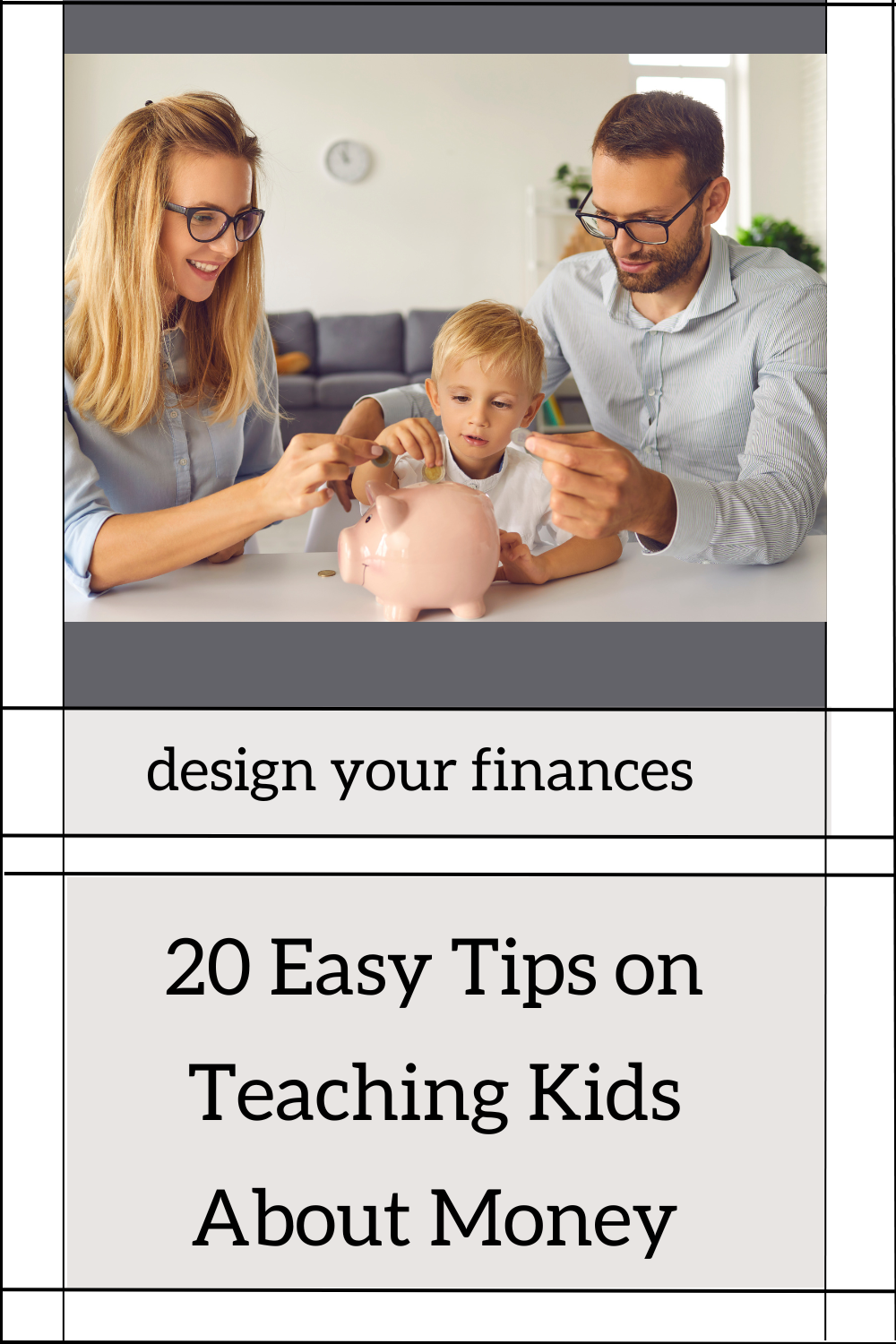

20 Easy Tips on Teaching Kids about Money

Teaching Kids about Money early instills good financial habits and knowledge and it is essential for their long-term financial well-being.

Teaching Kids about Money early instills good financial habits and knowledge and it is essential for their long-term financial well-being. Financial literacy is an essential life skill that, when nurtured from a young age, can empower children to make informed and responsible financial decisions in the future. Teaching kids about money doesn’t have to be a complex or daunting task; in fact, it can be an engaging and enjoyable process for both parents and children. In this comprehensive guide, we will explore 20 easy and effective tips to help parents, guardians, and educators teach kids about money. From setting up allowances and savings accounts to introducing the concept of budgeting and the value of delayed gratification, these tips are designed to create a strong foundation for financial understanding in children. Whether your aim is to instill financial responsibility, encourage smart saving habits, or prepare kids for a financially savvy future, these insights will provide you with practical and age-appropriate techniques to make the learning process engaging and enjoyable. So, let’s embark on this educational journey and discover the 20 easy tips for teaching kids about money, setting them on the path to financial competence and independence.

.

1. Start Early

Starting early in teaching kids about money is crucial for their financial literacy and future financial success. By introducing basic money concepts and good financial habits from an early age, children can develop a strong foundation for making smart financial decisions.

- Two examples of starting early in teaching kids about money include providing an allowance and encouraging savings. Providing children with a regular allowance allows them to learn the value of money and the concept of budgeting. It gives them the opportunity to make their own spending choices and understand the consequences of their financial decisions.

- Encouraging savings by setting up a savings account or piggy bank helps children develop the habit of saving and understand the benefits of delayed gratification. It teaches them the importance of setting aside money for future goals and emergencies. By starting early and instilling these fundamental money concepts, children can grow up with a solid understanding of personal finance and develop healthy money management skills that will serve them well throughout their lives.

Begin teaching kids about money as early as possible to build a strong foundation for their financial literacy.

.

2. Use Everyday Opportunities

Using everyday opportunities to teach kids about money is an effective approach in fostering their financial literacy and understanding of personal finance. By incorporating money-related discussions and activities into their daily lives, children can develop practical money skills and learn important financial lessons.

- Using everyday opportunities in teaching kids about money include involving them in grocery shopping and encouraging them to save for a specific item. Involving children in grocery shopping trips provides an opportunity to discuss budgeting, comparison shopping, and making informed purchasing decisions. Parents can discuss the cost of items, explain the importance of price comparisons, and involve children in deciding what to purchase within a set budget.

- Encouraging children to save for a specific item they desire, such as a toy or game, teaches them the value of setting goals, patience, and saving money over time. Parents can help children calculate how much they need to save, set a savings timeline, and celebrate the achievement once the goal is reached. By utilizing everyday opportunities to teach kids about money, parents can create valuable learning experiences and empower children to make wise financial choices throughout their lives.

Utilize everyday situations like grocery shopping or budgeting for family activities to teach kids about money management.

.

3. Set an Example

Setting an example is a powerful way to teach kids about money and instill good financial habits. Children observe and learn from their parents’ behaviors and attitudes towards money, making it essential for parents to demonstrate responsible financial practices.

- Teaching kids about money include practicing smart spending habits and saving regularly. By demonstrating wise spending habits, such as budgeting, prioritizing needs over wants, and making informed purchasing decisions, parents can show children the importance of being mindful with money. This can involve discussing family financial goals, involving children in decision-making processes, and explaining the reasoning behind certain spending choices.

- Additionally, regular saving is another important behavior to model. Parents can openly discuss the family’s saving strategies, explain the purpose and benefits of saving, and involve children in setting aside money for specific goals or future needs. By setting an example of responsible financial behavior, parents can inspire and guide their children towards a healthy relationship with money and empower them to make sound financial decisions in their own lives.

Model good financial habits and behaviors yourself as children learn by observing their parents’ actions.

.

4. Allowance and Chores

Consider giving children an allowance tied to age-appropriate chores to teach them the value of earning money and financial responsibility.

Allowance and chores can be effective tools in teaching kids about money and instilling a sense of responsibility and work ethic. Connecting money to chores helps children understand the connection between effort and reward, as well as the value of their time and skills.

- Using allowance and chores in teaching kids about money include establishing a chore system and encouraging savings goals. By establishing a chore system, parents can assign age-appropriate tasks to their children and link them to a monetary reward

- This helps children develop a sense of responsibility, accountability, and the understanding that money is earned through work. Parents can also set clear expectations and rewards for completing chores consistently and to a satisfactory standard.

By incorporating allowance and chores into the teaching of money, parents can instill valuable lessons about work, money management, and financial responsibility in their children.

.

5. Saving Jars

By utilizing saving jars, parents can provide hands-on experience in money management, financial goal-setting, and the development of wise spending habits for their children.

- Saving jars are physical containers that children can use to allocate their money into different categories, such as saving, spending, and giving.

- This allows children to visually see how much money they have in each category and make informed decisions about how to allocate their funds. It fosters a sense of responsibility, planning, and awareness of where their money is going.

This teaches them the importance of patience, delayed gratification, and achieving financial milestones.

.

6. Goal Setting

Goal setting is a fundamental aspect of teaching kids about money and cultivating their financial literacy. By setting clear goals, children can learn the importance of planning, discipline, and delayed gratification.

- Incorporating goal setting in teaching kids about money include saving for a specific purchase and setting long-term financial goals. Saving for a specific purchase, such as a toy or gadget, allows children to experience the satisfaction of working towards and achieving a short-term goal. Parents can help their children set a realistic savings target, track progress, and celebrate the accomplishment once the goal is reached. This exercise teaches children the value of saving, budgeting, and making conscious choices with their money

- Additionally, setting long-term financial goals, such as saving for higher education or a future investment, instills a sense of responsibility and a forward-thinking mindset. Parents can engage their children in discussions about long-term financial goals, help them understand the steps required to achieve those goals, and encourage regular savings towards them.

By incorporating goal setting into financial education, parents empower their children to develop a proactive and purposeful approach to managing their money and working towards their aspirations.

.

7. Money Discussions

Having open money discussions is a crucial aspect of teaching kids about money and fostering their financial literacy. Regularly engaging in conversations about money helps children develop a healthy understanding of financial concepts and attitudes towards money.

- Involving children in family financial decisions and discussing money values. Involving children in family financial decisions, such as budgeting or major purchases, provides them with a real-world context to understand the practicalities of money management. Parents can explain their thought processes, involve children in decision-making discussions, and answer their questions about money-related matters. This promotes transparency, critical thinking, and financial awareness.

- Discussing money values, such as the importance of saving, giving, and responsible spending, helps children develop a strong foundation for making ethical and responsible financial choices. Parents can have age-appropriate conversations about the value of money, the difference between needs and wants, and the significance of being mindful with finances. By fostering open money discussions, parents can empower their children to become financially responsible individuals with a strong understanding of money and its role in their lives.

Engage in age-appropriate conversations about money, explaining basic concepts like earning, spending, saving, and investing.

.

8. Budgeting Basics

Introduce the concept of budgeting by involving kids in creating a budget for family expenses or their own purchases. Teaching kids about budgeting basics is a fundamental step in their financial education journey. Budgeting helps children understand the concept of income, expenses, and making informed choices with their money.

- Teaching budgeting basics in relation to money include creating a spending plan and tracking expenses. Creating a spending plan involves helping children allocate their money into different categories, such as saving, spending, and giving. Parents can provide a visual representation, such as a simple budgeting sheet or envelopes labeled with different categories, to help children see where their money is going and make conscious decisions about how to allocate it.

- Tracking expenses involves keeping a record of money spent on various items or activities. Parents can encourage their children to track their purchases, either by using a notebook or a budgeting app, to understand where their money is being spent and identify areas where they can make adjustments. This practice helps children develop awareness of their financial habits, prioritize their spending, and make adjustments as needed.

By teaching kids budgeting basics, parents empower them to develop responsible money management skills that will benefit them throughout their lives.

.

9. Delayed Gratification

Teach children the value of delayed gratification by encouraging them to save for something they really want instead of instant impulse purchases.

- Delayed gratification in relation to money include saving for a larger purchase and setting financial goals. Encouraging children to save for a larger purchase, such as a toy or gadget, teaches them the value of setting aside money over time instead of impulsively spending it. This experience demonstrates the rewards that come with delayed gratification and helps children understand that waiting and planning can lead to more satisfying outcomes.

- Discussing the importance of consistent saving and long-term planning, children learn to prioritize their future financial well-being over immediate wants. This practice cultivates a sense of responsibility and helps children develop the habit of making thoughtful financial decisions.

By emphasizing delayed gratification, parents can equip their children with a valuable skill that can positively impact their financial choices and overall well-being throughout their lives.

.

10. Comparison Shopping

Involve kids in comparing prices and making informed purchasing decisions to develop their critical thinking skills. Teaching kids about comparison shopping is an important lesson in financial literacy that helps them become savvy consumers.

- Comparison shopping involves evaluating different products or services to find the best value for money. By teaching children this skill, parents can instill the importance of making informed purchasing decisions and stretching their dollars.

- Researching prices involves teaching children to compare prices of similar items across different retailers or online platforms. Parents can involve children in the process of finding the best deal by discussing factors like quality, features, and price.

- Reading product reviews helps children understand the importance of gathering information and considering the experiences of others before making a purchase. Parents can encourage children to read reviews from reliable sources or even involve them in writing their own reviews after purchasing a product.

By incorporating comparison shopping into their financial education, parents equip children with the skills to evaluate options, make cost-conscious decisions, and develop a critical mindset when it comes to spending money.

.

11. Banking Basics

Teaching kids about banking basics is an essential component of their financial education. Understanding how banks work and the various banking services available can help children develop responsible money management habits.

- Opening a savings account allows children to learn firsthand about the process of depositing money, tracking their balance, and the benefits of saving. Parents can take their children to a bank or credit union, explain the purpose of a savings account, and guide them through the steps of opening their own account.

- Introducing the concept of interest helps children understand how their money can grow over time. Parents can explain how interest is earned on savings accounts and discuss the concept of compound interest, which encourages long-term saving habits.

- Parents can involve children in monitoring their account statements and discussing the growth of their savings through interest.

By teaching banking basics, parents empower their children to become financially literate individuals who can navigate the banking system confidently and make informed decisions about their money.

.

12. Allow Mistakes

Let children make small financial mistakes and learn from them. It helps them develop resilience and better decision-making skills. Allowing mistakes is an important aspect of teaching kids about money and fostering their financial independence.

- Allowing mistakes in teaching kids about money include giving them control over a budget and allowing them to make purchasing decisions. Giving children control over a budget means providing them with a certain amount of money and allowing them to make decisions on how to spend or save it.

- If they make a mistake, such as spending all their money too quickly, they can experience the consequences firsthand and learn the importance of budgeting and planning. Allowing children to make purchasing decisions on their own, within reasonable boundaries, also allows them to learn from their mistakes.

- For example, if they buy a toy impulsively and later regret it, they can learn the importance of thoughtful spending and the value of considering their needs and wants before making a purchase. By allowing mistakes, parents provide a safe environment for children to learn and grow, teaching them resilience, responsibility, and the skills necessary for making informed financial decisions in the future.

Mistakes provide valuable learning opportunities and teach children the consequences of their financial decisions.

.

13. Charity and Giving

Encourage children to donate a portion of their money to a cause they care about, fostering a sense of empathy and generosity. Teaching kids about charity and giving is an essential aspect of their financial education and nurturing their sense of empathy and social responsibility. Instilling the value of giving back to others helps children develop a compassionate and generous mindset.

- Teaching charity and giving in relation to money include encouraging children to donate a portion of their allowance and involving them in volunteer activities. Encouraging children to donate a portion of their allowance teaches them the importance of sharing their resources with those in need. Parents can discuss different charitable organizations or causes and allow their children to choose where to direct their donation.

- Involving children in volunteer activities, such as participating in food drives or helping at local community centers, provides them with firsthand experiences of giving back and making a difference in their community.

Parents can engage children in discussions about the importance of helping others and the power of collective action. By teaching charity and giving, parents nurture their children’s empathy and encourage them to be thoughtful and compassionate individuals who positively contribute to society.

.

14. Money and Entrepreneurship

Inspire entrepreneurial skills by encouraging kids to start small businesses or participate in money-making ventures, such as a lemonade stand. Teaching kids about money and entrepreneurship is a valuable way to foster their financial literacy and entrepreneurial skills. Introducing the concepts of business, earning income, and financial independence at a young age can ignite their creativity and ambition.

- Encouraging them to start a small business or engage in entrepreneurial activities and teaching them financial management within their business. Encouraging children to start a small business, such as a lemonade stand or a crafts store, provides them with firsthand experience in generating income, managing expenses, and understanding the value of their products or services.

- This allows them to develop skills in budgeting, marketing, customer service, and problem-solving. Teaching financial management within their business involves guiding children in tracking their revenue, expenses, and profits. Parents can explain concepts like profit margins, reinvesting in the business, and saving for future goals.

By teaching kids about money and entrepreneurship, parents empower them to explore their passions, develop important life skills, and cultivate a mindset of financial independence and creativity.

.

15. Online Safety

Teaching kids about online safety is crucial when it comes to their financial well-being and protecting their personal information. In today’s digital age, it’s important for children to understand the potential risks and how to navigate the online world responsibly.

- Teaching online safety in relation to teaching kids about money include educating them about secure online transactions and promoting responsible social media usage. Educating children about secure online transactions involves teaching them about the importance of using secure websites when making online purchases.

- Parents can explain the significance of looking for the padlock symbol or “https://” in the website address to ensure encrypted connections for safe transactions. It’s also important to teach them to keep their personal and financial information confidential, including passwords and account details.

Parents can emphasize the importance of privacy settings, caution against oversharing personal details, and encourage children to think critically about the information they share online. By teaching kids about online safety, parents help them become responsible digital citizens, protect their financial information, and navigate the online world with confidence.

.

16. Investing Basics

Introduce basic investment concepts in an age-appropriate manner, teaching kids about the potential benefits, risks of investing and how to build credit the right way

- Teaching kids about money include explaining the concept of compound interest and introducing them to the stock market. Explaining compound interest involves teaching children how their money can grow exponentially over time through the power of compounding. Parents can illustrate this concept by showing how even small regular contributions can accumulate significant wealth over long periods.

- Introducing kids to the stock market can be done by explaining the concept of buying shares of companies and potentially earning returns on those investments. Parents can use age-appropriate resources, books, or games to introduce the stock market and help children understand the basic principles of investing in stocks. By teaching investing basics, parents equip children with the knowledge and mindset to make informed investment decisions, develop long-term financial goals, and build wealth over time.

Understanding the fundamentals of investing helps children develop a long-term perspective and a foundation for building financial security.

.

17. Financial Literacy Resources

Utilize books, online games, and educational resources specifically designed for teaching kids about money and finance.

Financial literacy resources play a vital role in teaching kids about money and equipping them with the necessary knowledge and skills for financial success. These resources provide valuable educational materials, activities, and tools that can make learning about personal finance engaging and accessible.

- Use financial literacy resources for teaching kids about money include online platforms and interactive mobile applications. Online platforms dedicated to financial literacy for kids offer a wide range of resources such as educational articles, videos, interactive games, and downloadable worksheets. These platforms often present financial concepts in a fun and age-appropriate manner, making it easier for kids to grasp and apply the knowledge.

- Interactive mobile applications designed for kids can also provide engaging financial lessons. These apps often feature interactive games, simulations, and quizzes that teach kids about budgeting, saving, and making smart financial decisions.

These resources not only make learning about money enjoyable for kids but also empower them with the foundational knowledge and skills needed for a lifetime of financial well-being.

.

18. Allow Kids to Make Decisions

Give children opportunities to make financial decisions within a controlled environment, allowing them to learn from their choices. Allowing kids to make financial decisions is an essential aspect of teaching them about money and fostering their financial independence. It empowers them to take ownership of their financial choices and learn from the consequences of their decisions.

- Giving them a budget for purchasing their own clothes and toys and involving them in family financial discussions. Giving kids a budget for purchasing their own clothes and toys allows them to make decisions within the boundaries of their allocated funds.

- They can learn the value of money, practice making choices based on their priorities, and experience the trade-offs involved in their spending decisions. Involving kids in family financial discussions, such as budgeting or planning for a vacation, enables them to understand the financial aspects of everyday life.

They can contribute ideas, learn about budget constraints, and participate in decision-making processes. This involvement helps them develop critical thinking skills and a sense of financial responsibility. By allowing kids to make decisions, parents promote their financial autonomy, encourage responsible money management, and prepare them for future financial independence.

.

19. Encourage Saving for the Future